A Spendthrift Trust is a type of Asset Protection Trust designed to safeguard trust assets from creditors, lawsuits, and imprudent spending by your beneficiaries. By placing restrictions on your beneficiary’s access to trust funds, Spendthrift Trusts help ensure your assets are preserved and distributed according to your intent — rather than being subject to external claims or poor financial decisions.

Spendthrift Trusts are commonly used when your beneficiary may be vulnerable to financial mismanagement, creditor pressure, substance abuse issues, or undue influence. They can also be effective in protecting your inheritances from divorce settlements, judgments, or aggressive creditors, depending on applicable law and trust structure.

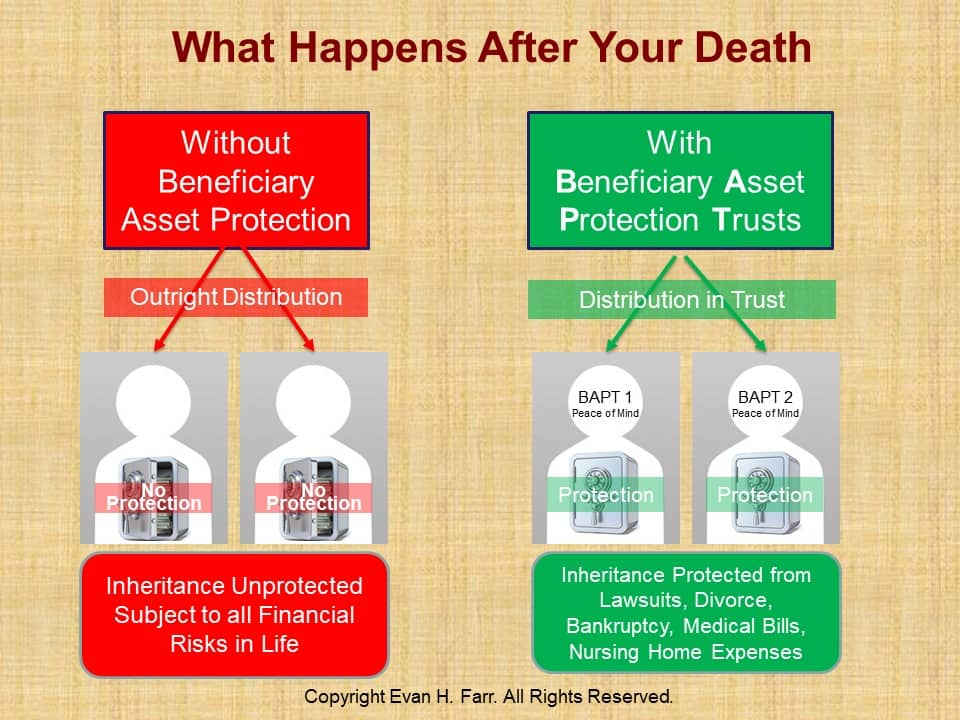

Please note that a Beneficiary Asset Protection Trust is known by many other names, including a Spendthrift Trust, a Discretionary Trust, an Inheritance Trust, and a Dynasty Trust. What you call it makes no difference in the protection it provides.

How Do You Establish a Beneficiary Asset Protection Trust / Spendthrift Trust / Dynasty Trust / Inheritance Trust?

As Virginia estate planning lawyers, Maryland estate planning lawyers, and DC estate planning lawyers, one of the strategies that we often recommend to our clients is the Beneficiary Asset Protection Trust (also called a Spendthrift Trust or Dynasty Trust or inheritance trust), which we can build into your Revocable Living Trust or your Living Trust Plus Asset Protection Trust, to take effect upon the death of the trust creator. Whether your trust is created in Virginia, Maryland, or DC, a Beneficiary Asset Protection Trust / Spendthrift Trust / Dynasty Trust / Inheritance Trust creates a sub-trust for each beneficiary. Typically, the beneficiary of each sub-trust acts as his or her own trustee and can use the assets in the trust for his or her own health, education, maintenance, and support (the latter two — maintenance and support — encompass almost anything). If you have beneficiaries who you’re afraid will be irresponsible in managing their own sub-trusts (or if a beneficiary is or becomes subject to a lawsuit or judgment or under attack from other potential creditors), then a responsible third party — another family member or a professional trustee — can be named to act as trustee of a sub-trust to manage and disburse the funds in accordance with your desires as the creator of the trust.

What are the benefits of a Beneficiary Asset Protection Trust / Spendthrift Trust / Dynasty Trust / Inheritance Trust?

The beneficiary can have direct control of the assets as trustee of his or her own sub-trust, but the assets are protected from divorce, lawsuits, bankruptcy, and medical bills. The beneficiary can purchase assets in his or her name as trustee of the sub-trust. This can include primary homes, second homes, rental property, vacation property, land, vehicles, etc. — anything that has a title can be titled in the name of the sub-trust and protected inside the sub-trust.

If you don’t trust the beneficiary to act as the trustee, then you can name a different trustee who can make direct payments to landlords, mortgage lenders, schools, doctors, hospitals, etc. Or the trustee could make regular payments to the beneficiary, similar to an allowance.

Can a Beneficiary Asset Protection Trust / Spendthrift Trust / Dynasty Trust / Inheritance Trust Fail or Be Thwarted?

Although the Beneficiary Asset Protection Trust may be the best solution for people who want to protect inheritances for their beneficiaries, or who have fiscally irresponsible beneficiaries, there are several ways a Beneficiary Asset Protection Trust can fail or be thwarted:

Beneficiary Acting as Trustee Removes the Assets: If the beneficiary is serving as the trustee of his or her own trust, the beneficiary could thwart the protection of the trust by distributing assets out of the trust and into the individual name of the beneficiary. Worse yet, the beneficiary could then commingle those distributed assets to a joint account with a spouse or another individual, thus possibly subjecting those assets to divorce and/or to lawsuits or other creditor attacks against the joint account owner.

Trustee’s Actions: If you are not using a professional trustee, such as a qualified trust company or an experienced Virginia trusts and estates attorney or Maryland trusts and estates attorney or DC trusts and estates attorney, as the trustee of the Spendthrift Trust, you should be careful that the person you pick will make the best decisions for your beneficiary. Simply put, trusts may not work well if the trustee doesn’t do a good job. For example, the trust may not work well if your trustee doesn’t use a professional money manager or distributes too much money to your beneficiary or refuses to make appropriate distributions to the beneficiary or commits outright fraud or embezzlement.

Exempted Creditors: In some states, certain entities are not considered creditors and can access funds in the trust, even though they might have to go through the courts. For instance, a parent seeking child support or an ex-spouse who is owed alimony may be allowed to bring suit to access the funds in the trust. Some states also allow creditors who provide “necessary” goods and services — such as food, housing, and medical care — to go after funds in the trust. Lastly, the IRS can sometimes go after money in a spendthrift trust. This IRS Memorandum explains that the IRS may levy on certain assets of the trust, despite the existence of spendthrift provisions, if the taxpayer possesses fixed and determinable property rights in the trust. A levy will seize the taxpayer’s fixed right to trust income and the taxpayer’s fixed right to obtain a future distribution from the corpus. Also, if a trustee distributes funds that the trustee knows are encumbered by a federal tax lien, the trustee can be liable for tortious conversion, i.e., intentionally impairing the security of the IRS lien.

Are There Laws Specifically Allowing Beneficiary Asset Protection

Yes. In many states, there is case law supporting the use of Beneficiary Asset Protection Trusts / Spendthrift Trusts. In many states this case law, called common law, has also been codified into a statute, often specifically stating that the beneficiary can also be the trustee of his/her own Beneficiary Asset Protection Sub-Trust. For example:

Virginia Law “Virginia Code § 64.2-746 Discretionary trusts; effect of standard” states as follows: E. A creditor may not reach the interest of a beneficiary who is also a trustee or cotrustee, or otherwise compel a distribution, if the trustee’s discretion to make distributions for the trustee’s own benefit is limited by an ascertainable standard.

Maryland Law “14.5-510. Ability of creditor to attach, exercise, reach, or otherwise compel distribution of interest in trust” states: Interests of beneficiaries that are trustees or sole trustee of trusts but not settlors of trust (a) A creditor may not attach, exercise, reach, or otherwise compel distribution of the beneficial interest of a beneficiary that is a trustee or the sole trustee of the trust, but that is not a settlor of the trust, except to the extent that the interest would be subject to the claim of the creditor were the beneficiary not acting as cotrustee or sole trustee of the trust.

Spendthrift Trusts may help you:

- Protect your assets from your beneficiary’s creditors

- Control the timing and purpose of distributions

- Preserve your family wealth across generations

- Reduce the risk of misuse or rapid depletion

- Provide long-term financial stability and oversight for your beneficiaries

In your Spendthrift Trust, the trustee — rather than your beneficiary — controls distributions, guided by standards you set forth in the trust document. This structure allows your assets to be used for appropriate purposes such as education, housing, long-term care, or general support, while preventing direct access that could expose your funds to risk.

Spendthrift Trusts are often incorporated into your broader estate and asset protection plans. They can be combined with discretionary trusts, Special Needs Trusts, or family trusts to address your specific goals and circumstances. Proper drafting is critical, as the effectiveness of your Spendthrift Trust depends on precise language, trustee selection, and compliance with state law.

When designed thoughtfully, your Spendthrift Trust balances protection with support — providing your beneficiaries with resources while preserving your assets and honoring your long-term family objectives.

Why Choose Farr Law Firm

Farr Law Firm brings experience and strategic insight to spendthrift trust planning.

- Asset Protection Experience: The firm understands how spendthrift provisions function under Virginia, Maryland, and DC law.

- Customized Trust Design: Each trust is tailored to the beneficiary’s needs and the grantor’s goals.

- Integration With Estate Planning: Spendthrift Trusts are coordinated with wills, living trusts, and legacy strategies.

- Risk-Aware Structuring: Emphasis on enforceability and long-term effectiveness.

- Clear, Practical Guidance: Clients receive straightforward explanations of complex trust mechanisms.

Protect Assets while Providing Responsible Support

A Spendthrift Trust can help protect assets while ensuring beneficiaries receive support in a structured, responsible way. Farr Law Firm provides experienced guidance to help you determine whether this strategy fits your planning goals. Contact us today to discuss Sspendthrift Trust planning tailored to your needs.

Farr Law Firm Locations

Farr Law Firm proudly serves clients throughout the region, with offices in: